A more precise approach to EBT fraud prevention

Fraud in Focus: Balancing access and security through out-of-state and online transaction controls

EBT programs are expanding, and so are the risks that come with them.

Online purchasing, cross-state usage, and broader access have improved how residents receive benefits. At the same time, they’ve introduced new vulnerabilities that fraud actors are actively exploiting.

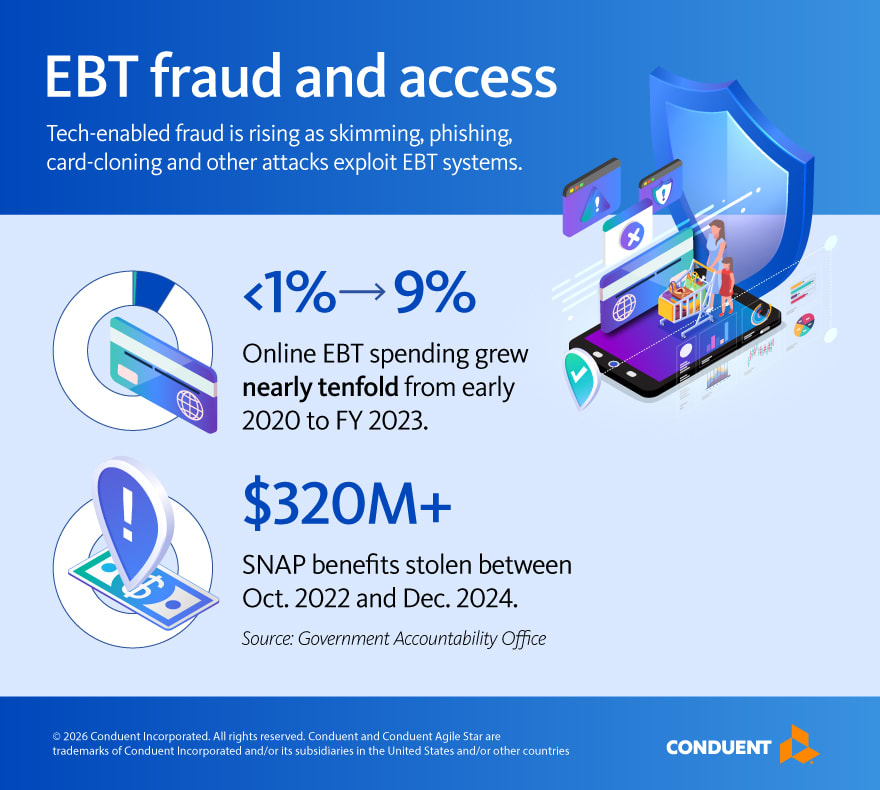

According to the United States Department of Agriculture, online EBT spending grew from less than 1% of total transactions in early 2020 to nearly 9% by fiscal year 2023. What began as a limited pilot has since scaled nationwide, permanently changing how and where benefits are accessed.

That expansion improved access for residents who could not easily reach physical retailers and made benefits more usable in everyday life. But it also introduced a new environment for fraud, and what was once a localized risk became distributed.

The expanding fraud surface

As access points increase, fraud risks expand across more places and channels. Fraud schemes now span both physical and digital channels. In-store skimming devices still capture card data. At the same time, more advanced methods are emerging. These include account takeover, credential harvesting, and exploitation of online retailer systems.

The Government Accountability Office has found that fraud increasingly relies on technology. Skimming, phishing, card cloning and automated bot attacks are now common tactics. These approaches allow fraud to scale quickly, often draining benefits before detection.

States have already felt the impact. More than $320 million in stolen SNAP benefits were replaced between October 2022 and December 2024 due to electronic theft.

How transaction blocking changes the model

Out-of-state and online transaction blocking allows agencies to define where and how EBT cards can be used based on risk. Instead of waiting for fraud to occur, transactions can be restricted in high-risk geographies or channels before losses happen.

This approach introduces a simple but important shift. It moves fraud prevention upstream.

Rather than relying solely on investigations and reimbursements, states can reduce exposure at the point of transaction. Fewer fraudulent transactions occur. Fewer claims need to be processed. Fewer residents are impacted.

Balancing protection with access

Stronger controls only work if they maintain access.

Transaction blocking is designed to be flexible. States define baseline protections, but cardholders can remain active participants. When legitimate needs arise, such as travel, cardholders can temporarily adjust their settings where permitted.

This shared responsibility model improves adoption and trust. It ensures that fraud prevention supports access instead of limiting it.

It also reflects a broader shift in program design. Security is no longer something that happens behind the scenes, but something residents can see and influence.

What early implementation shows

Initial state implementations point to measurable impact.

Cardholder protection increased significantly following rollout, with some programs seeing protection levels rise by roughly 300%, according to internal Conduent research. Blocked transaction dollars also increased sharply, in some cases by about 500%, compared to prior approaches that relied only on card lock and unlock features.

Adoption has remained high. More than 90% of active cardholders consistently used high-risk transaction settings after implementation. States that invested in upfront education saw smoother transitions and fewer disruptions in benefit usage.

Where this fits: A layered approach with VeriSight

Out-of-state and online transaction blocking is part of a broader fraud prevention strategy. Conduent’s VeriSight Anti-Fraud Solutions bring these controls together into a layered defense model. Transaction blocking complements capabilities such as EMV chip enablement, high-risk transaction controls and account-level protections like card lock and unlock and suspicious terminal blocking. Together, these measures reduce exposure across both physical and digital channels.

The goal is not a single control. It is coordinated protection.

By combining multiple safeguards, states can address fraud at different points in the transaction lifecycle. This layered approach helps reduce losses, limit disruption, and strengthen overall program integrity without requiring system replacement.

Related: Brochure: Conduent VeriSight Anti-Fraud Suite

What cardholders can do

Cardholders play a direct role in protecting their benefits. Simple actions can make a measurable difference. Locking cards when not in use helps reduce exposure. Monitoring account activity allows for a faster response. Staying engaged with available fraud tools strengthens overall program protection.

When states and residents work together, fraud becomes harder to execute and easier to contain.

A more resilient path forward

Fraud tactics will continue to evolve. EBT programs must evolve with them.

Out-of-state and online transaction blocking is one piece of a broader strategy. It adds a proactive layer that reduces risk without limiting flexibility. It helps states protect benefits earlier in the process, where it matters most.

In a more complex fraud environment, the goal is not to eliminate access. It’s to protect it with precision.

Learn more

Explore how Conduent helps states strengthen EBT fraud prevention, or reach out to an expert.

- Conduent Expands Deployment of EBT Solutions to Prevent Fraud and Improve Customer Experiences Across U.S. States

- Reducing theft of SNAP benefits: A smarter path to prevention

- Partnering with the U.S. Secret Service to fight EBT fraud

- Two states leading the way in SNAP EBT modernization, fraud prevention